Technology

1 min read

Why legacy Compliance fails in the New Age

Legacy compliance assumes slow rules and annual filings. Article explains why technology-led, system-aligned compliance is now critical to get and stay compliant

Roopali Grover

Section 2(y) of the Code on Wages, 2019, works as a small engine, an inclusive core, 7 exclusions and 3 governors. Learn the engine to classify pay component

Roopali Grover

Editor

Before the four labour codes, “wages” meant slightly different things in the Minimum Wages Act, the Payment of Wages Act, the Payment of Bonus Act and the EPF and ESI statutes. A payroll team could legitimately compute one base for provident fund and another for gratuity. The Code on Wages, 2019 ends that fragmentation: one definition, in §2(y), now feeds every downstream calculation — minimum wages, overtime, bonus eligibility, PF and gratuity base, retrenchment compensation, leave encashment and inspection assessments.

That single point of control is why the definition is worth understanding structurally rather than as a memorised table. Get §2(y) right once and the whole compliance cascade follows. Get it wrong and the error propagates everywhere at once.

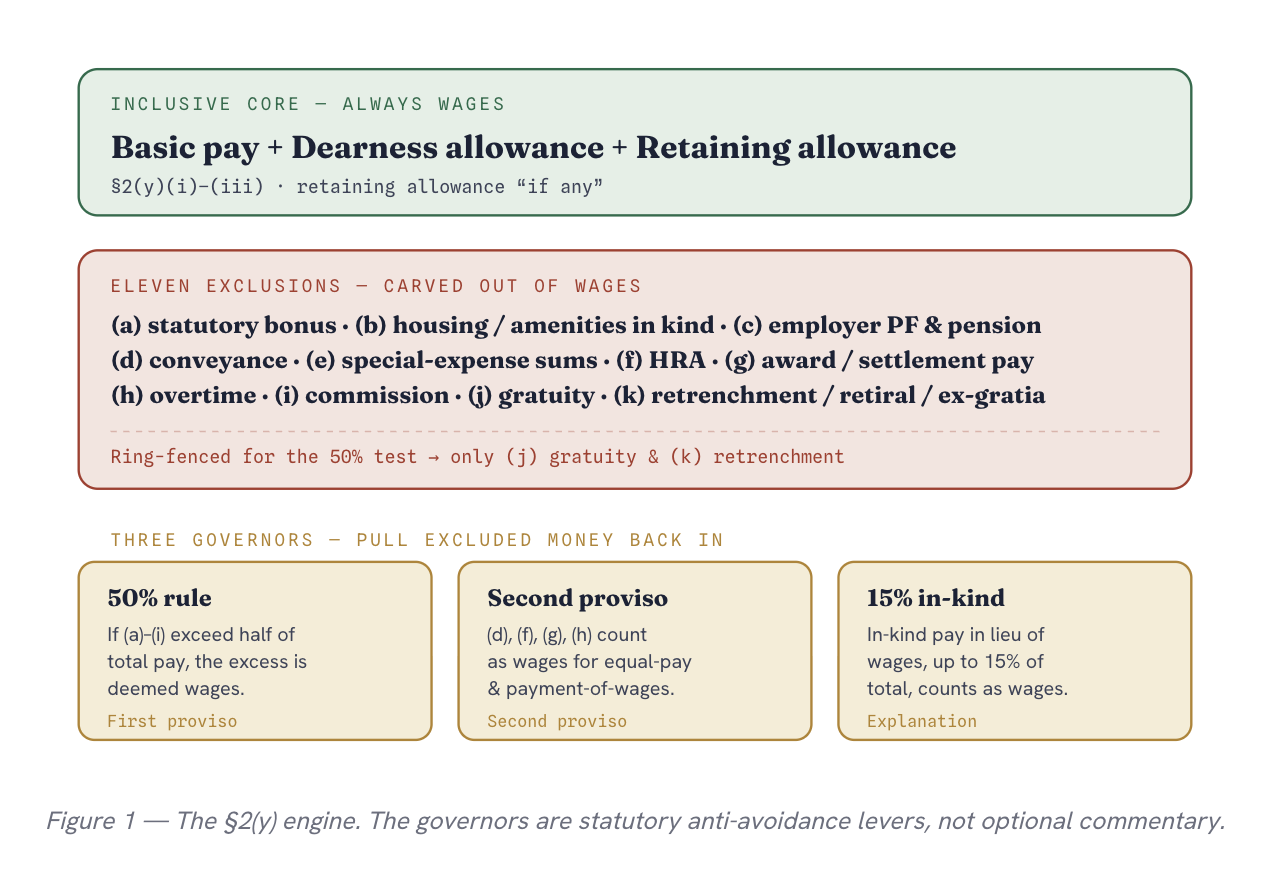

01 / The model Three parts, working together

The text of §2(y) reads as one long sentence, but it has a clean internal architecture. There is an inclusive core that is always wages; an exclusion list of eleven items, lettered (a) to (k); and then three governors, provisos and an explanation that pull some excluded money back into wages under defined conditions. The governors are the part most tables ignore, and they are where the compliance risk lives.

02 / The core, What is always wages

The opening limb of §2(y) defines wages as all remuneration, by way of salary, allowance or otherwise, expressed in or capable of being expressed in money, payable to a person for their employment, and it expressly includes three things: basic pay, dearness allowance, and retaining allowance, if any.

These are the bedrock. Nothing in the rest of the section can carve them out, and the governors below exist mainly to stop the core from being hollowed out by relabelling. A retaining allowance, paid to keep a seasonal or intermittent worker on the books between active spells, sits in the core only where one is actually paid, hence the statutory “if any”.

03 / The exclusions, The eleven carve-outs, (a)–(k)

After the inclusive limb, §2(y) lists eleven categories that are not wages. Reading them in order is worth the minute it takes, because the lettering matters for the governors that follow. Clauses what are excluded:

Written by

Roopali Grover

Editor at RGA

Structured Approach

A systematic legal operations framework drives measurable business outcomes.

Automation First

Automation eliminates manual bottlenecks and accelerates execution across teams.

Strategic Value

Legal operations transforms from a cost center into a competitive advantage.

The detail almost everyone misses. The 50% test below operates only on clauses (a) to (i). Clauses (j) gratuity and (k) retrenchment / retiral / ex-gratia are terminal, separation-linked payments — they are fully ring-fenced and never added back, however large they are. Treating “all exclusions” as the basis for the 50% calculation, as many summaries do, overstates the add-back.

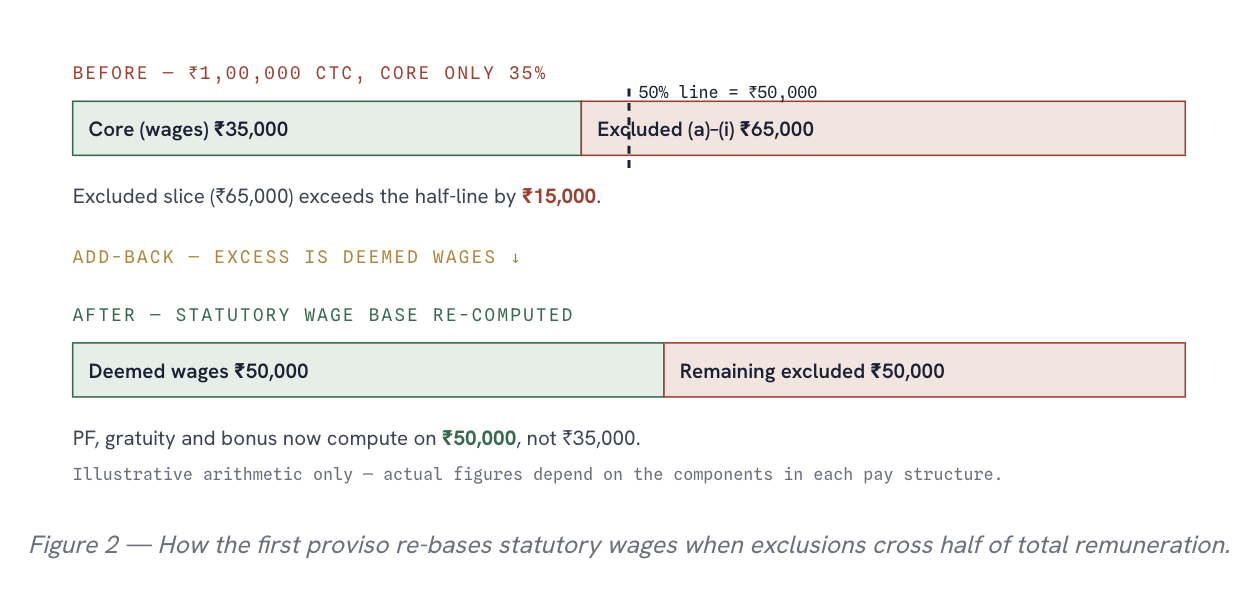

04 / Governor one, The 50% rule (first proviso)

This is the heart of the reform. The first proviso says that for calculating wages, if the payments under clauses (a) to (i) exceed one-half, or such other percentage as the Central Government may notify, of all remuneration, then the excess over that half is deemed to be wages and added back.

In practice this sets a floor: the inclusive core (basic + DA + retaining allowance) must come to at least half of total pay. The classic structure of a 30–40% basic with the balance loaded into allowances no longer holds, because the moment the excluded slice crosses 50%, the overshoot is re-counted as wages and inflates the PF, gratuity and bonus base anyway.

Grey zone — variable pay. Performance incentives and variable pay are not given their own exclusion clause. Where such a payment is genuinely a commission it falls under (i); a statutory bonus falls under (a). Anything that fits neither tends to be treated as an excluded component that still counts toward the 50% test — so it cannot be used to escape the floor. The conservative reading is to include variable pay in the denominator and watch the half-line.

05 / Governor two, The second proviso — context-specific add-backs

This is the governor most “included vs excluded” tables drop entirely, yet it changes the answer for two purposes. The second proviso provides that for equal remuneration across genders, and for the payment of wages, the emoluments in clauses (d) conveyance, (f) HRA, (g) award/settlement pay and (h) overtime are taken into the computation of wages.

So a component’s classification is not absolute, it is purpose-dependent. HRA is excluded for the PF and gratuity base, but is counted when testing equal pay between genders or when computing what must be paid out as wages. A correct compliance matrix therefore has a column for purpose, not a single yes/no per component.

06 / Governor three, The 15% in-kind rule (Explanation)

The Explanation to §2(y) addresses non-cash pay. Where an employee is given remuneration in kind, meals, free goods, gift vouchers and the like, in lieu of the whole or part of their wages, the value of that in-kind remuneration, up to 15% of total wages, is deemed to form part of wages. This stops employers from substituting cash wages with benefits beyond a modest ceiling. Note the framing: it is in-kind pay given in lieu of wages that is captured, not every perquisite an employer happens to provide.

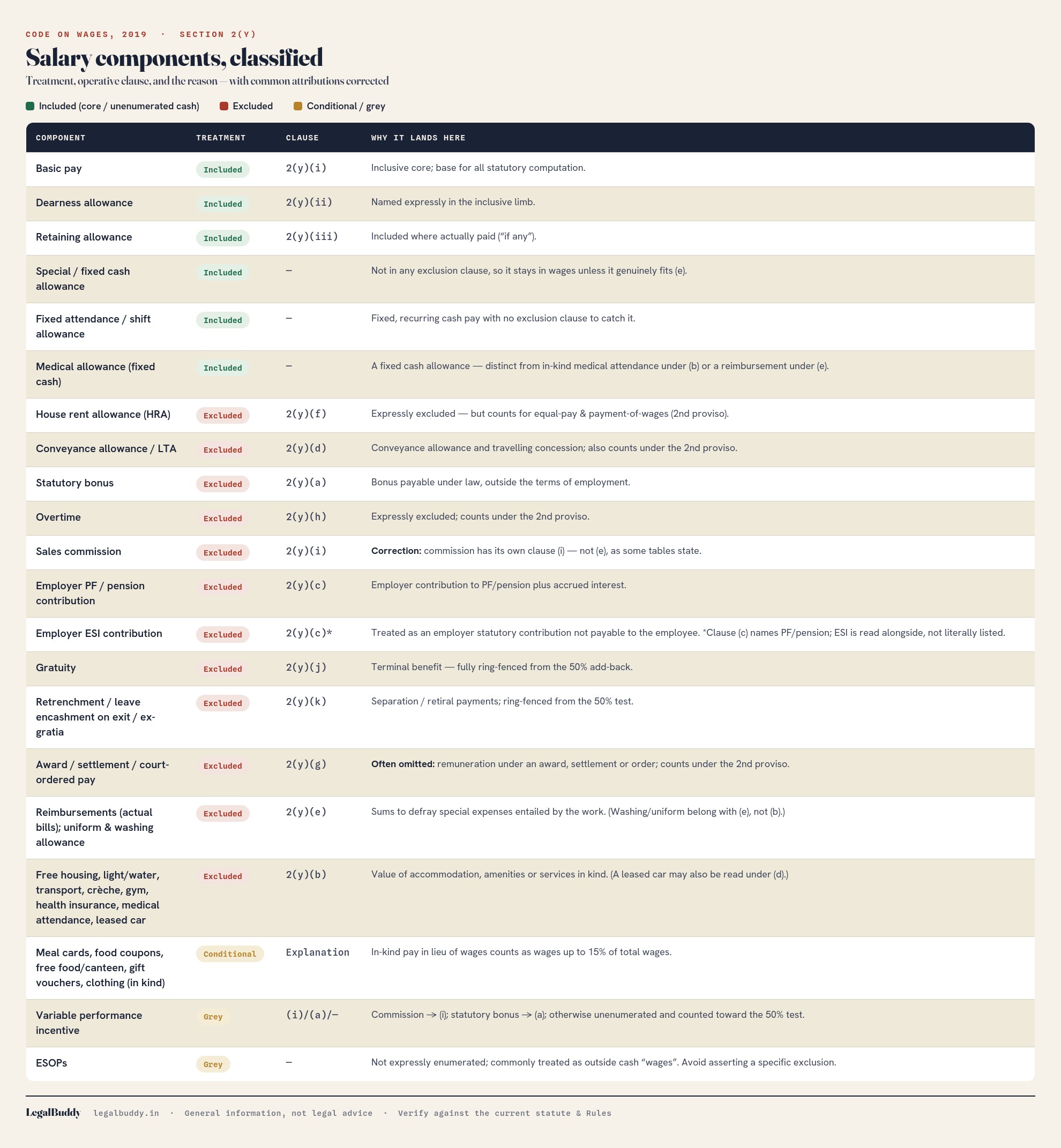

07 / The map, Components, classified, with corrections

With the engine in view, the table below sorts common CTC components, gives the operative clause, and says why each lands where it does. A few entries correct attributions that circulate widely in payroll summaries.

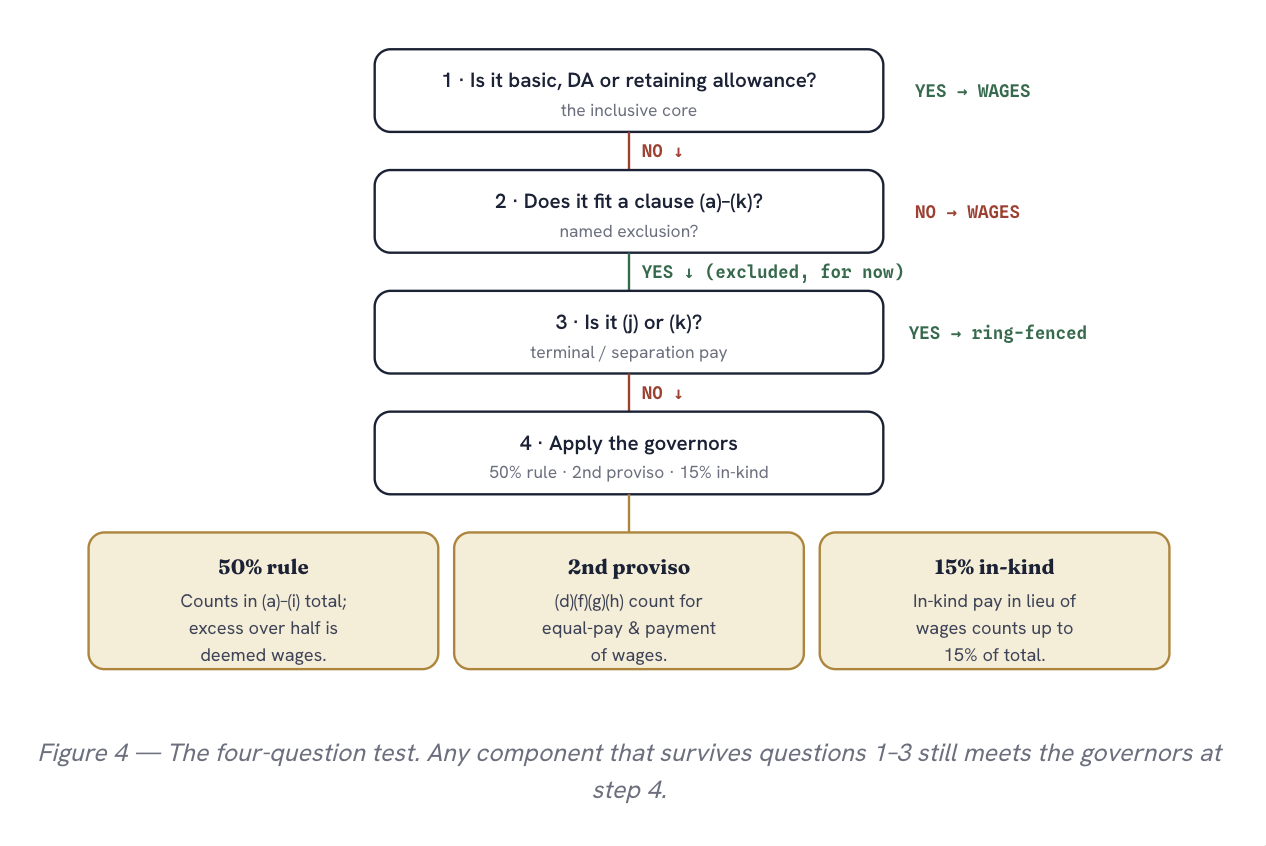

08 / The test, Classify any component in four questions

Rather than reach for the table, you can run any line item through the engine directly:

09 / In practice, What the structure asks of employers

The engine view points to a short, concrete checklist rather than a one-off relabelling exercise:

Re-base, don’t rename. Because the 50% rule re-counts the overshoot anyway, simply renaming allowances achieves nothing. The durable fix is to lift the inclusive core to at least half of total pay.

Model the cascade. A higher wage base raises PF, gratuity provisioning and bonus exposure together. Quantify the combined effect before restructuring, not after.

Build a purpose-aware matrix. Thanks to the second proviso, the same component answers differently for the PF base, for equal-pay testing and for payment of wages. Encode the purpose, not just the component.

Update the paperwork and registers. Appointment letters, CTC templates and the wage and overtime registers maintained under the Code on Wages (Central) Rules, 2020 should reflect the re-based structure and the in-kind ceiling.

CCPA penalises seller for non-BIS toys sold online. Key lessons for retailers on due diligence, BIS compliance and marketplace liability.

Roopali Grover